Tax Return Filing for Non-residents

(Real Estate Rental and Leasing Industry)

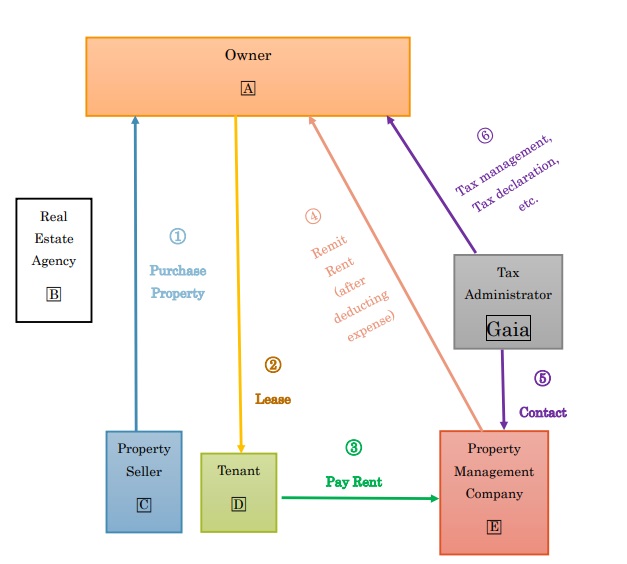

1.Basic Transaction Illustration

2. Business Proces

Step 1 request the income and expenditure report from the management company or the owner of the property

Step 2 Make a statement of income and expenditure

Step 3 collect relevant vouchers of income and expenses

Step 4 make, review and confirm the declaration form

Step 5 Make a tax report to the customer via Emai

Step 6 Submit a confirmation statement

Step 7 Pay taxes or collect repayment